Why not repay relatives before filing bankruptcy? This post addresses a situation where you borrowed money from a relative before bankruptcy. Many people do this in an attempt to keep from having to file for bankruptcy. But often, the money borrowed from the relative isn’t enough to prevent the inevitable.

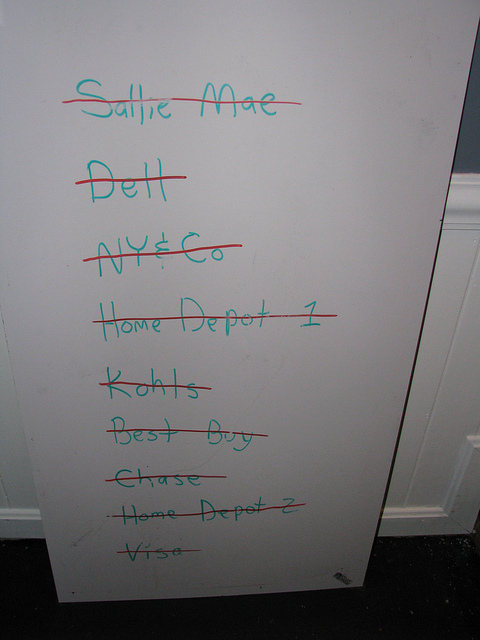

The general rule about repaying creditors before bankruptcy can be stated as follows: If, before you file a bankruptcy, you pay a creditor more than you are paying at that time to your other creditors, then that favored creditor may have to return the money so that it is shared among all your creditors.

This is especially true if you are paying one creditor when you are no longer paying anything to anyone else. The payment to your favored creditor is called a “preferential payment”—you are considered to be paying that creditor in “preference” over your other creditors.

Unfortunately, the good intentions you had in repaying a creditor may backfire, especially if that creditor – the person to whom you owed the money – is a family member. That’s because repaying a relative within the year before filing for bankruptcy can get that family member mixed up in your bankruptcy case. Your relative may have to fork over the money to your bankruptcy trustee—even if that money has already been spent.

The trustee may well sue your family member to get that money, which is something that bankruptcy law allows the trustee to do. And afterwards, assuming that you feel a moral or family obligation to make that person whole, you would be paying that debt a second time after your bankruptcy is done.

The good news is that this problem can be avoided if you get good legal advice before you make the “preferential” payment or series of payments to that favored creditor. Even if you’ve already made that payment or series of payments when you see your attorney for the first time, there are often ways to get around it.

Watch out – the law about preferences is complicated. Section 547 of the Bankruptcy Code, while by no means the most confusing one in the code, is still unclear. It’s about 1,318 words long, containing 56 sub-sections and sub-sub-sections. If you look at it, I think you’ll agree that this is NOT a do-it-yourself aspect of bankruptcy law.

So IF there is a chance that you will need to file a bankruptcy, BEFORE you pay anything to a relative or any other kind of special creditor that you feel duty-bound to pay, FIRST talk to an experienced bankruptcy attorney. Do so even if—in fact especially if–you don’t consider the person you’d like to pay a “real” creditor, because, for example, the debt was never put in writing, or nobody knows about it.

And most importantly, if you HAVE made such a payment before you see your attorney, be sure that you disclose this information to the attorney at the beginning of your first discussion. It may well affect the timing of your bankruptcy filing. Preferences are mostly a problem when they are discovered AFTER the bankruptcy is filed. That’s what you want to avoid most. Avoid that and it’s possible that preferences will not be a problem for you.

If you’re thinking about filing for bankruptcy in New Jersey, call Jennifer N. Weil, Esq. at (201) 676-0722.

Photo by kevin dooley.